Introduction

For countless centuries economists have tried to successfully analyse so many, countless , fallacies (like the great depression and how the consumption function works , how to reduce unemployment without causing any cyclical fluctuations ) although many theories have been propounded for these circumstances , as such there is no clear cut or straight jacket explanation. One such “circumstance” is Switzerland’s Negative interest rate policy (NIRP), many economists have been trying to figure out how Switzerland’s economy is still functioning under these circumstances. In this report we will see what relation interest rate has on investment and how the central bank can manipulate interest rate to control investment. In the next section we will see what NIRP is in a broader aspect. In the last section we will study the case of the country under study (Switzerland) and its NIRP and the resultant “Frankenshock”.

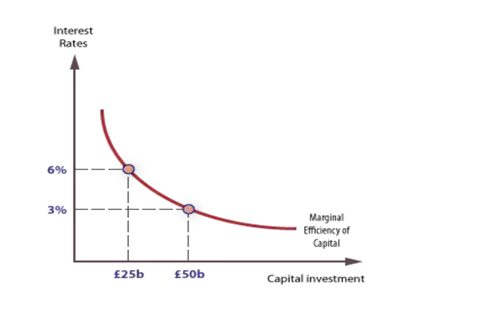

Interest rate and Investment

To understand the negative interest rate policy we must first understand what kind of relationship between investment and interest rate. Interest rate manipulation is a very important tool used by the central bank of a country to control aggregate demand by directly affecting the investment. Interest rate and investment have an inverse relationship in terms of cost of borrowing and at times opportunity cost. For an investment to happen the individual in question would require funds and we shall assume that he wants to acquire these funds from the bank. If the bank has a high interest rate the individual would feel discourage to invest as the cost of acquiring these funds is very high and at times higher than the proportional profit the person would earn. A lower interest rate in effect would encourage investment as the cost of procuring these funds are low ( the individual has to pay a lower amount of interest). In terms of opportunity cost, a higher interest rate would attract the individual to deposit his money in the bank (safe and assured return in terms of interest received ) instead of investing ( comparatively riskier). As such we can see that the relationship between Interest rates and Investment is inverse.

If the central bank feels that the economy is experiencing recessionary trends or feels that the aggregate demand is too low it can reduce the interest rates thereby inducing investments are as such increase the aggregate demand and vice versa.

Negative Interest Rate Policy

A negative interest rate policy (NIRP) is an unusual financial arrangement instrument utilized by a national bank whereby nominal target rates are set with a negative value, beneath the hypothetical lower bound of zero percent. A NIRP is a generally new improvement (since the 1990s) in monetary policy approach.

A negative interest rate implies that the central bank (and maybe private banks) will charge a negative premium. Rather than accepting cash on deposits, depositors must pay normally to keep their cash with the bank. This is expected to boost the lending activities of the banks and to encourage investments and effectively discourage people to hold money in the banks. During deflationary periods, individuals and organizations hold cash as opposed to spending and investing. The outcome is a breakdown in the total aggregate demand, which prompts prices to fall much further, a log jam or stop in real output and expansion in the unemployment rate. A free or expansionary monetary strategy is normally utilized to manage such monetary stagnation. Notwithstanding, if deflationary powers are deep-rooted and strong, cutting the national bank’s loan cost to zero may not be adequate to invigorate borrowing and lending.

Negative loan costs can be viewed as a final desperate attempt to support monetary development. Essentially, it’s established when all else has demonstrated incapable and may have fizzled. Hypothetically, focusing negative interest rates will diminish the expenses to acquire funds for organizations and family units, driving demand for loans and boosting investment activities and consumer spending.

Frankenshock

On January 15 (2015) the Switzerland national bank announced a very shocking and bold move regarding its interest rates. It is a known fact that lower interest rates induce investments and raise the aggregate demand. The SNB took this policy to another level by reducing the interest rate below zero to -0.75 %. In theory this policy should push or encourage investment limitlessly( or to a great extent). The reason for this attempt is most probably to avoid or remove any deflationary situations. This policy was not predicted by anyone and was very suddenly introduced , much like our “demonetization” by our Prime Minister.

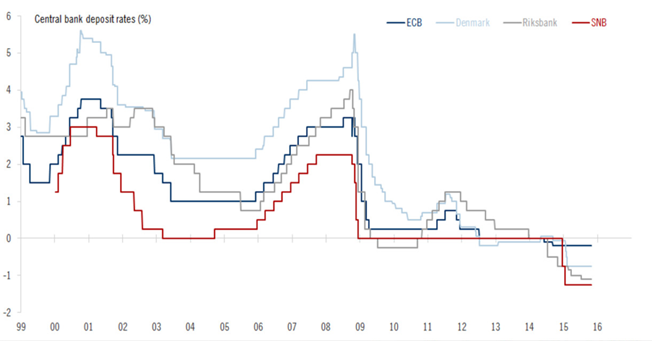

From the graph above we can infer that Switzerland always had a low interest , at least lower comparatively lower than the rest , the reason for this could be that Switzerland always had a problem with depression and wanted to use expansion policies to induce inflation to deal with the depression. We can see other countries follow the same policy too, however we will focus only on the country under study.

The banks are having a huge problem with keeping up with the costs of this NIRP(negative interest rate policy) and the increase in value of the franc makes it worse for them to keep up with the costs. Reports have said that the cost of maintaining the negative interest rates on deposits was nearly 1 billion Francs and this was just a part of the burden.

This new policy also has a negative impact on the profitability of these banks as the interest earned by these banks are a huge source of income for the banks and this policy curbs their profit by reducing their interest margins. Therefore banks are finding it very hard to compete and as such survive in that environment.

There is mass uncertainty in markets because of this new and sudden policy. Insurance companies have gained the upper hand in the mortgage business. There are too many existing investors and due to the new policy more investors have been attracted , the problem here being too less investment opportunities. The higher value of the Franc has resulted in a decline in exports and as such reduced the revenue earned in comparison to cost. As such the entirety of the export industry has suffered major losses.

Even after such consequences this country’s financial system has been functioning rather smoothly , markets clear and the swiss banks net income increased in the past years

They were able to control the value of their currency and the GDP of the country also increased. The swiss bank knew the dangers and the costs of the negative interest rates and as a compensation for that, they expanded the mortgage market.

Conclusion

We have seen the relationship between interest rate and investment , and have also studied how a country can implement NIRP and still function properly. Now the important question is , is Switzerland an example of how a country can efficiently use the negative interest rate policy or is this just a fluke?. Well, from my point of view although the currency shocks were not considered by the SNB , I feel like the cause for this policy to not throw the entire economy into a world of hell is mainly due to Switzerland’s existing market forces and their relative stability. The SNB played a vital role in diverting its attention towards expanding the mortgage market so as to compensate for the banking sector loss. Taking Switzerland as an example many European countries are planning to implement the same (to what extent is unknown). It is still a mystery as to how the Swiss economy is continuing to function under these circumstances and is in fact one of modern day economic fallacy.

References

- Bassetto, M. (2004). Negative Nominal Interest Rates. The American Economic Review, 94(2), 104-108. Retrieved from http://www.jstor.org/stable/3592865

- Levy, M., Levy, H., & Avi Edry. (2003). A Negative Equilibrium Interest Rate. Financial Analysts Journal, 59(2), 97-109. Retrieved from http://www.jstor.org/stable/4480470

- https://tradingeconomics.com/switzerland/interest-rate

- https://perspectives.pictet.com/2015/10/28/qa-on-the-ecbs-negative-rates-its-decision-to-cut-rates-again-should-be-fx-dependent/

- https://www.bloomberg.com/news/articles/2019-03-19/world-s-lowest-interest-rate-brews-trouble-for-swiss-property

Wonderful analysis and really smart presentation. Even a non economics person would love it .

LikeLike

Very well done. A really interesting read.

LikeLike

Thank you. It was very interesting to read

LikeLike

very interesting and comprehensive, good job!

LikeLike